Is the Middle Class Still Attainable?

Gen Z's Economic Struggle

One critique of our cultural moment is the unattainability for young people of the American dream, or what we might more accurately call the middle class — which for shorthand I’ll define as the cost, relative to income, of owning a home and modest, reliable transportation. Is the malaise of much of Gen Z due to moral defects, as some members of older generations claim, or is this malaise simply a rationalization of basic economic hurdles to what came easier in previous eras?

As one of the youngest cohorts of Gen X, I entered real adult life around the year 2000. In January 2001, the median home price in the United States was about $140,000, according to the National Association of Realtors, whereas median household income was around $42,000 according to the Census Bureau. This gives a ratio of 3.33. Modest, reliable transportation, which I’ll define as a Toyota Corolla, had a new MSRP of about $13,000. Thus the total cost of a “starter life” was about 3.64 times the annual median income.

In September 2024, the median price of a home was $404,500. The cheapest Toyota Corolla has an MSRP of $22,000. Median household income was $80,610 in 2023, and bumping this 3% to estimate a 2024 figure yields around $83,000. The “starter life” to median income ratio has risen to 5.14; I’ll call this the “Life Difficulty Index.” Things are indeed much more expensive for the rising generation, and this is without considering their increased student loan burden.

Note also that young people starting out are unlikely to earn the median income. This means that small changes in the costs of a basic life can quickly price out many from their attainment.

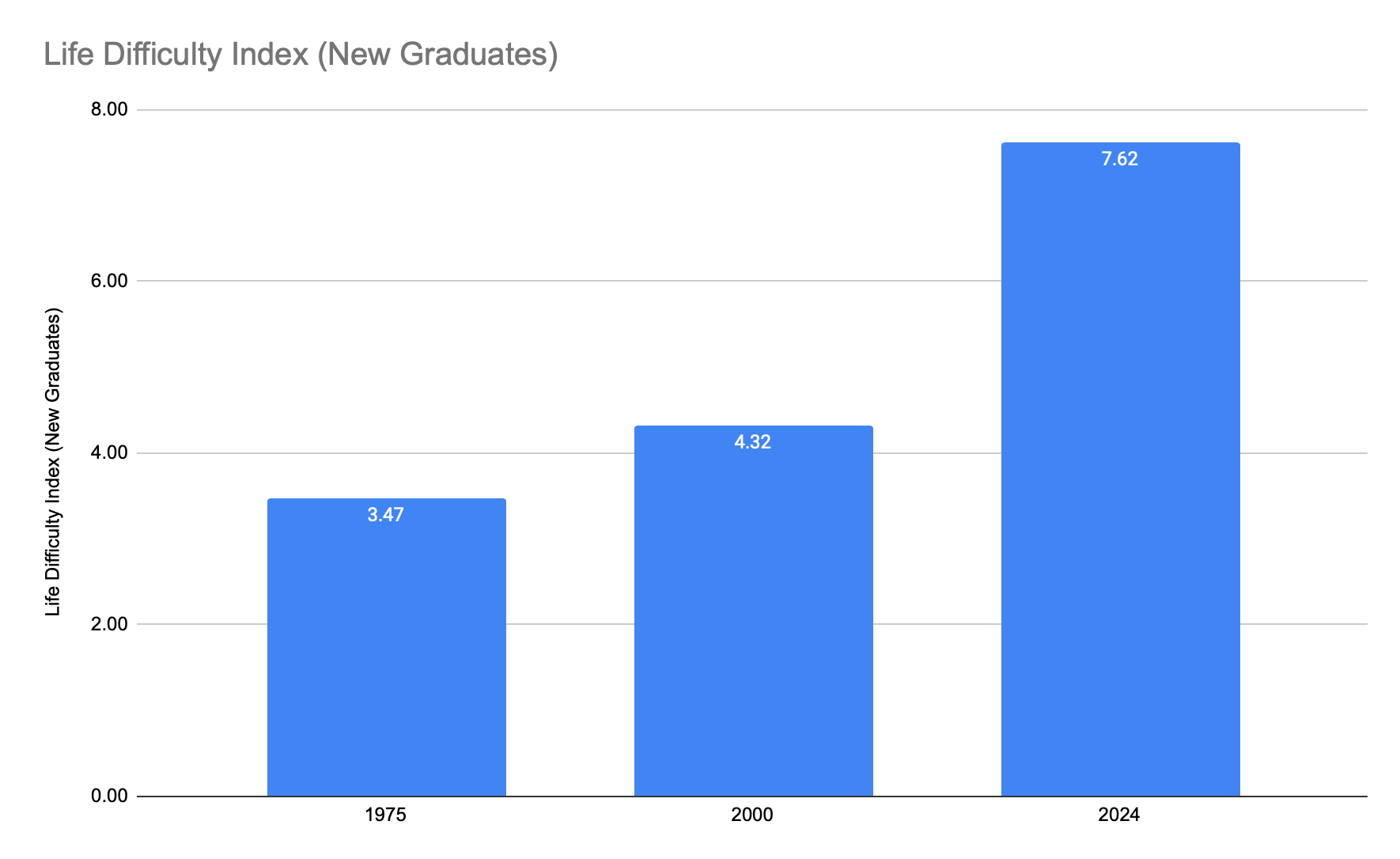

The average starting salary for college graduates in 2000 was $35,400, somewhat less than the median income. In 2023, the average starting salary for college graduates was around $56,000. So while the cost of housing has tripled and the cost of transportation has almost doubled, salaries are only up 58% in nominal terms. Recomputing the ratios above for college graduates yields 4.32 and 7.61, respectively, or a 76% increase in costs.

Incidentally, the Toyota Corolla was introduced to the US market in 1975, just as the youngest Boomers were emerging into adulthood. If we crunch the same numbers for that year — new graduate starting salary of $12,095, median home price of $39,300, and Corolla MSRP of $2,711 — we can compute a new college graduate Boomer Life Difficulty Index of 3.47. Here’s a comparison of these generations separated by about a quarter century (spreadsheet for reference here):

Late Generation X had it 24% harder than the Boomers, and today’s graduates face a market where a middle-class life is more than double, about 120% more, difficult to achieve than it was for late Boomers in 1975.

CPI Quality Adjustments

Interestingly, between 2000 and 2023, inflation was “only” 77%, yet the costs outlined above clearly more than doubled, while salaries have lagged even nominal inflation. Do we believe our lying eyes or government inflation statistics? Maybe both, if we account for what the government calls “hedonic quality adjustments.”

According to the government, part of the increased cost of goods today is not inflationary because those goods are of higher quality. Both houses and Toyota Corollas are larger and more feature-rich than 25 years ago. An example is provided here, where it is demonstrated that a 3.6% annual increase is reduced to 0.66% when adjusted for new features.

If we look at the historical CPI index for new vehicles, we see that the latest figure is 177, compared to 142 in the year 2000, or a nominal price increase of only 25%, not the actual 69% increase in Corolla’s sticker price. The new Corolla, according to the government, only really “costs” $16,250 because it provides so many more features.

The CPI is adjusted similarly for housing, which is calculated as “owner’s equivalent rent,” or the amount of rent the owner of a home avoids net of costs. From 2001 to 2025, the index went from 202 to 415, or a 102% increase, compared to the actual cost of a median home increasing by 188%. Square footage is also a factor, as the median home in 2000 was about 2,000 SF versus (as best I can tell from sources) around 2,300 SF in 2023, or a 15% increase. Independent of size, the CPI is still assuming that a home today represents an increase in quality and thus hedonic value of 62%!

415 / (202 * 1.15) = 1.78 (Square footage adjusted owners’ equivalent rent ratio, nominal)

$404,500 / $140,000 = 2.89 (increase in median home price ratio, nominal)

2.89 / 1.78 = 1.62 (inferred ratio of quality adjustment)

To be fair, owners’ equivalent rent is not the same as the median home price, and rents have not kept up with housing prices (more on that shortly).

The Detailed Math Doesn’t Matter

We can debate whether these quality adjustments are real. What isn’t debatable is that the entry-level or hurdle for affording a middle-class lifestyle has gone up significantly.

Ultimately, people don’t really care if their car has more airbags and a backup camera, or if their house if more energy efficient. What they care about is whether the money they earn is sufficient to allow them an independent life and not feel like a loser compared to their parents at comparable ages. And the numbers show that’s about 76% harder than it was a mere 23 years ago when I began my adult life.

Earlier I cited starting salaries for college graduates. Some have posited that credential inflation has cheapened the value of college degrees, with one recent study showing college graduates now having IQs (~102) just slightly higher than the population average, and declining by about 0.2 IQ points per graduating class. College enrollment rates have increased from somewhere around 35% to 39%. This, however, does not strike me as fully explaining the decline in affordability.

We can test this by looking at engineering graduates, one of the few academic disciplines that has not declined in rigor1. Around the time I graduated in chemical engineering, average salaries were $53,000 per year. At the same school today, they’re $90,000, or a 70% nominal increase, which is almost in line with inflation at 77%. This compares to 58% for college graduates in general. So it’s plausible that both declining academic standards and a broader student population, and thus a cheapening of the quality of graduates in both capability and skills, explains some of this gap.

If we redo the calculations above for engineering graduates, the Life Difficulty Index in 2000 was 2.89, compared to 4.74 today, only a 64% increase, somewhat better than the average, and probably much better in practice given many engineering jobs are located in low cost-of-living areas2.

Is This Sustainable?

The sustainability of this situation is questionable. In particular, it’s hard to imagine how the housing market can continue at its current heights without massive increases in wages or a decline in home values. But no matter which angle I look at it, I can’t devise a consistent hypothesis.

Housing prices are high, as are interest rates, but many houses still sell below replacement cost, which is the opposite of what one would expect if there was truly a bubble. Land, building materials, and labor have gone up during the same period. On the flip side, and this makes no sense to me as well, rents have not gone up as much relative to housing prices, which is a big reason why the CPI, in relying on rents as a proxy for housing costs, is lagging people’s actual experience on the ground.

Wages have grown somewhat as well, but the increase in real wages I found plausible when I reviewed The Great Demographic Reversal has yet to materialize. It seems companies continue to find ways to do more with fewer people, eating into their accumulated “BS Jobs” margin.

Most firms can just not hire people and get about the same amount done because the people there already accomplish so little, and reductions in staff relative to revenue drive a natural increase in efficiency. This is particularly true for new graduates, who beyond the cost of training often have severe emotional problems from parental coddling and growing up in the woke era.

The only explanation that makes sense for housing is a secular change in demand exceeding supply’s ability to compensate, and the explanation for that is the massive immigration of the Biden administration. These newcomers are not directly competing for the median home, but demand at the bottom filters its way to the top because ultimately every head needs a roof and must pay what they can afford to have it.

The increase in housing prices is due to the broadly wealthy upper middle class being able and then forced to pay more. The mainstreaming of calls for “mass deportation” this election cycle in Trump’s broad multi-ethnic coalition certainly feels like people realizing these costs have a specific cause rather than indulging in prejudice.

Yet, even this immigration explanation fails when it comes to rents not keeping up with housing prices, especially when new immigrants disproportionately rent. It’s truly an economic mystery, and why a housing crash can’t be ruled out, especially as Boomers pass away or enter long-term care and their homes come onto the market. In the long term, the price of a house ought to be a linear function of the rent avoided.

Implications

I like economic and/or biological explanations for social phenomena, as they are more subject to falsification than other hypotheses, but one must be cautious of either under or overplaying their significance. But if I allow myself to speculate, much of Gen Z’s difficulties can be seen as rationalizations of the expense of family formation.

A recent CNBC article highlighted the apparent disconnect between recent college graduates’ actual salaries and what they expected. Their expected salary, $85,000, is obviously well above market compensation. However, if it were, their “Life Difficulty Index” would approximate that of late Generation X (5.02 vs. 4.32).

Older generations can mock these inflated expectations all they want, but on a cost basis, these graduates aren’t asking for the moon, just for a shot at the kind of life college graduates could easily enjoy 25 years ago. It’s quite obvious, yet again, that our economy seems intentionally designed to harm young people for the benefit of older asset owners3.

The ancient psychological insight of Aesop about sour grapes seems appropriate here. If affording a normal family life seems impossible to achieve, why even try? Why work at all when food and video games are cheap and better than ever? If the old markers of status, a house, spouse, and children, are too expensive to achieve and woke culture condemns the normal and functional, why not adopt an alternative, sterile sexual lifestyle that marks one among the blessed rather than the cursed?

As I’ve raised teenagers, it’s become more obvious to me the importance of peers. I tell younger parents that their biggest leverage post-puberty is careful control (i.e. range restriction) of their child’s peers. Sex hormones change everything and orient young people towards the future, rather than the past, and they are ultra-sensitive to what attains status among their peers than what their parents think. More broadly, I think foundational economics influences this peer process in the culture.

The Mustang Effect

I call this the “Mustang effect,” which I’ll illustrate with an anecdote. A close male relative of mine was in high school in 1965, when the Ford Mustang, the affordable muscle car, was introduced. So enchanting was the Mustang marketing mystique that this young man dropped out of high school for a year to work at a grocery store to pay cash for a new Mustang, returning to school the following year with his baby blue pony car. At that time, the MSRP of a Ford Mustang was $2,427 and could be financed for $50 per month. The minimum wage in 1965 was $1.25, so a Mustang was just under 2,000 hours of labor. Today, by comparison, a Mustang starts at $32,000, and the minimum wage is $7.25 — or about 4,400 hours of minimum wage labor.

Now the economists computing the CPI can argue all they want about how much “better” the new Mustang is compared to the old one, but in terms of the currency young men care about, the cool factor, i.e. impressing girls, no one can seriously argue that the 1965 Mustang was somehow deficient in comparison, and probably more so given the car culture of the time.

In the 1960s and 1970s, in places like J.D. Vance’s hometown of Middletown, Ohio, 18-year-old teenage men were as foolish and impulsive as they are today. But what they observed is that their peers just a couple of years older than them could get a good factory job and afford muscle cars to impress the girls. That made staying at home, smoking weed, and generally being a loser a less attractive option. Similarly, young people in their early 20s, once they got tired of partying, could see a clear exit ramp to get married, buy a house, and raise a family among their peers just a bit older.

Once these jobs and factories left, and the prices of the basic capital goods of middle-class life inflated, there were fewer successful peers where the average young man could see himself succeeding if he would control his baser impulses of sloth and gluttony. While it cannot explain everything, I do not believe we should discount the effect of basic economic facts. The average person, in particular, makes decisions based on status incentives and then creates a moral framework to back-justify those decisions4.

Mitigation

Nationally, the Trump movement represents the resentment of average Americans who feel these frustrations. We can hope that a new industrial and immigration policy — and I would add a monetary policy5 that cares less about the net worth of older asset owners (let the housing market crash!) — can make the labor of the average American valuable enough again to afford a middle-class life. As Tucker Carlson once put it, his politics is whatever policies result in 100 IQ high school graduates being able to buy a house, two cars, and raise kids on a single income. We can wish the New Right good luck in achieving these goals long-term.

Hope, however, is not a strategy for individuals, and as the old market aphorism goes, “the market can stay irrational longer than you can stay solvent.” Given the limited window for young people to enter true adulthood, get married, and have kids, families need to think about mitigating strategies independent of what may or may not happen at a national political level.

Thoughts and recommendations:

There’s the possibility that the post-WWII middle class is an impossible-to-replicate historical aberration. The relative income equality and ability for people to accumulate assets independently with their own labor was in fact historically anomalous and may never return.

Recognize that life is objectively more difficult for young people today than it was 25-50 years ago. Help your kids, if you can, if they otherwise have good character, accumulate basic capital assets like cars and homes.

Be extremely cautious about debt for the depreciating asset of a college degree. If you can pay cash, fine, but outside of Tier One colleges, it’s almost always a mistake to borrow for education. Most people of above-average intelligence will still want to get a bachelor’s degree, particularly for licensed or technical professions, but those who aren’t wealthy should do it as cheaply as possible and pay-as-you-go6. Controlling for IQ, more selective colleges do not enhance earnings, and Ivy League applicants who are waitlisted earn about the same as those who are admitted. See my column here.

Consider multi-generational living arrangements. Most empty nesters have homes larger than they need, and historically, it was extremely common for young families to live with a set of grandparents when starting out. If you have land, consider building an empty nester cottage or “barndominium” for yourself and let the kids and grandkids live in the big house; they’ll get more utility out of the space anyway.

In all of this, it’s important to maintain a posture of humility. To help your kids effectively, you can’t make a big deal about the money, or attach too many strings. Acknowledge that they have it harder, and you’re helping them because you had it easier, and that the family supporting the younger generation isn’t charity, but a moral imperative, if the family is to have a future. Economically, that’s undeniable.

Finally, if you see a young family who is succeeding despite these hardships, know that, by the numbers, their character and drive are more than double that of equivalent Boomers, and at least 50% better than that of Generation X. They are probably having to sacrifice and watch every penny to a degree you can’t even imagine in your youth. Those members of Gen. Z who make it are impressive indeed.

A really smart freshman I know, with better entrance scores than mine, seems to be struggling almost as much as I did ~30 years ago with his first-semester weed-out engineering calculus class.

I know a young lady who, upon getting engaged to an engineer, was shocked when she learned how high his starting salary was at 22 years old compared to his peers and how she had expected to need to work but realized he would be able to support them both easily. She told me, “the cheat code to life is to just marry an engineer.” Boring and complicated careers also seem to have the lowest divorce rates.

My investing partner calls this “cynical optimism,” which he interprets as having a bias against the possibility of a systemic deflationary crash. We should assume, in making investments, that the system will always do whatever it can to protect the ruling class, i.e. leveraged asset owners. This is particularly true post-2008, when they figured out they can print money in a targeted way for their friends to support asset prices, and prevent the insolvency of leveraged economic incumbents, without causing hyperinflation.

The anxiety of today’s parents and kids, which exacerbates the problem of achieving independence through practices like helicopter parenting, can be seen as a rational reaction to on-the-ground economic facts. The immature orientation of many people in their 20s, of bringing their parents to job interviews and the like, can be interpreted as basic biology. In times of perceived scarcity, young animals retain juvenile behaviors longer to signal their need for resources from the providing parent.

This may be yet another justification for a “minimum interest rate” policy I advocated for in my review of The Price of Time. The same male relative I described above in the Mustang story was able to build a small 2-bedroom home for cash while working a blue-collar job in the late 1970s. The extremely high interest rates of that era made materials, land, and labor for home building super cheap. High interest rates are a boon to the frugal and virtuous and punish the profligate and foolish.

Loved this. And some of the best parts were footnotes.

Loved "the cheat code to life is to just marry an engineer". My mother-in-law did. My wife did. My daughter-in-law did.

I would paraphrase your article like this:

If housing is an investment, then within a few generations, the rising generation is priced out. We are there now.

Got your post from Aaron Renn, btw. Just subscribed.

Housing is the real bugbear here.

It's kind of like the "perfect storm" of factors, which is why I think it is hard to solve. Among these:

1. The increased cost of adding to housing stock relative to earlier eras (mostly due to regulation, but also NIMBY-type blocking), which tends to make the new housing disproportionately higher-end;

2. The increased importance of living in one of the "bubble" metropolises that took place during the period from 2000-2020;

3. The spread of some of the bubble population to other, smaller, cities throughout the country in the wake of the COVID lockdowns, which had the effect of "spreading" the increased cost of "bubble" housing to a wider number of markets than previously;

4. A very long period of historically low interest rates, which tended to drive up housing sale prices (more affordable than at higher rates);

5. The rise of widespread real estate investment in the residential housing market, which has tended to reduce supply of house for sale, and therefore pushing up prices; and

6. The short-term issues created by the sudden, sharp rise in interest rates (near doubling for mortgages in many places), which has created strong disincentives for existing owners to sell (they currently have low rate mortgages and do not want to replace them with high rate mortgages), which constrains supply and drives up prices.

Overall, there are a lot of factors that have worked to reduce the supply of "starter" housing, which has tended to increase the purchase cost of the existing housing stock. This has benefited existing owners at the expense of new entrants, and the effect is substantial, when you look at the cost of purchasing a home even over the past ten years (and the trend is longer than that). This has been turbo-charged by the sharp increase in mortgage rates since 2022, which has, in many places, effectively frozen the housing sales market (other than for people who are literally forced to move) -- another severe constraint on supply which places even more upward pressure on prices.

It's really just a perfect storm of factors weighing on supply that has sent the housing purchase market into a very dysfunctional place.

Rents have stopped increasing as much, it's true. It's not clear why, as you write. My own guess is that it may have something to do with how the residential sales market has gummed up. Fewer people are moving, more people are sitting still, including renters. That may mean less steep rental increases, because the demand overall for rentals isn't increasing that quickly as compared with a normal market where a lot of people are moving all the time and there is a brisk demand for rental units. Immigration should be creating upward pressure on rents, but it hasn't done so ... perhaps because the housing stock involved for that segment of the market is very low end, and therefore has a lesser impact on the prices at the mid and higher ranges of the market? I suppose it's also the case that, at least when it comes to rentals of single family homes, the increased supply of rental houses available, relative to purchasable houses, as a result of number "5" above, has tended to increase the supply, which tends to weigh on rents, at least for that segment of the rental market.