Prices, Discount Rates, and Profits

Prices, Discount Rates, and Profits

Mechanics of Christian Capitalism

This post is a continuation of an excerpt from an unpublished manual on my philosophy of business. Part One here.

How is it that capitalism provides for human needs better than any other system? So far, we have discussed the necessary preconditions for capitalism, notably security in peaceful enjoyment and improvement of private property which allows the meek (or self-controlled) to displace the aggressive in leading society.

Why is it that when we take this logic one step further and allow caring and intelligent people to simply plan economic production under systems like communism, poverty inevitably is the result? After all, capitalism seems to produce a good bit of waste.

One way to conceptualize the capitalist system is as one giant distributed network of agents incentivized to identify human needs and meet them. Central planning cannot possibly efficiently digest all of the needs of people from easily ascertained first principles. The economy is too complex and dynamic to be modeled that way.

Just as artificial intelligence only took off once coders gave up on trying to program rules and instead designed simple signal processing units that collectively solve complex problems based on feedback and learning, an economy’s needs can only be met by distributing the burden of information processing necessary to determine what needs to be produced, when, and by whom.

The Price Signal

Capitalism works because of a very simple, universal, and elegant mechanism: the price signal. This of course presupposes a form of money and currency, the debate over which is outside the scope of this book and is subject to a great deal of controversy1.

The price signal provides all participants in the marketplace with information indicating the level of human need for particular goods. Those who can produce those goods below the market price will generate a profit and increase production, while those whose costs exceed the market price will end production and find a more useful way to direct their productive efforts. The profits of a business, then, indicate the usefulness of its production to the rest of humanity, and thus the value of the business itself. Capitalism and profits, then, harmonize our interests and the interests of others, enabling us to truly love our neighbor as ourselves.

To this, we must add a few caveats. First, this is true in the very long run. In the short run, capitalism is subject to various manias of greed and fear that are economically irrational. Thankfully, however, this irrationality is limited to willing participants who risk their own capital, unlike central planning where bureaucrats without skin in the game can ruin an entire economy. If people wish to invest in foolish ventures that never produce a cumulative net profit, capitalism allows them, and the losses they eventually earn on that investment will send a useful price signal about future bad investments.

Second, I do not believe profits to be a universal indication of value like many libertarian idealists. Some profits cater to sin and vice, which create indirect externalities, and others have direct externalities, which are costs that neither the buyer nor the seller bear in the transaction. For example, a chemical plant dumping toxic waste products into a public waterway saves the buyer and seller money at everyone else’s expense. The hidden cost of the transaction is paid by society at large. Similar externalities occur with low-wage immigrant labor, especially in countries like the United States with significant social welfare systems2. Similarly, abusive alcohol consumption, which provides profits to alcohol producers, imposes hidden costs on families and productivity.

Externalities are best addressed with prohibitions where possible and regulations and taxes where prohibition is not practical. If not for federal excise taxes, for example, a gallon of vodka would cost $3 like a gallon of vinegar. Regulating the sale and cost of alcohol will tend to limit its harmful effects on society. Such a regulation protects legitimate, moderate use because the taxes are small and reasonable while making it at least inconvenient and somewhat unaffordable to abuse regularly. These regulations are ultimately judgment calls best informed by practical experience, not easily reduced to simple ideological principles. But these examples are exceptions, not the rule.

Marginal Economics

Profits do normally provide the most useful signal for the most valuable marginal good one can do for one’s fellow man in the economy. What do we mean by marginal? This concept is so important that we must enter into an extended discussion.

The purpose of the economy is to improve man’s material condition. Taking dominion over creation is not a random process, but a semi-ordered sequence, governed by price and profit signals, directing market participants to which resources would be most valuable to produce next, at the margin. Marginal value says little about absolute value, and the distinction is subtle but important.

For example, farming today is a very low-profit area of the economy. Farmland income yields (the ratio of net farming income generated to land value) are somewhere around 2-3%. A $1 million farm in land value might only produce $20,000 a year in income, a poverty wage for most families. Now this is a landlord’s yield net of labor costs, so if the farmer performed the labor personally this income might triple to $60,000. This farmer is a millionaire on paper but earns $20,000 on his investment while buying himself a $40,000-a-year job3. Even then, all of the profits would, in most years, be due to government subsidies for crop prices. Now a simplistic, absolute value thinker might say, “How very noble to meet my fellow man’s basic needs as a farmer.” And indeed, food has a very high absolute value, in that it is an absolute necessity for our survival.

The question in economics, however, is never what is good or bad in the abstract, but what an individual economic actor chooses as his or her next action. The extremely low yields, prices, and profits in the farming sector indicate we have more farmers than we need, which is why the economy is signaling that another marginal farm would add close to zero value, and thus do close to zero social good, and in fact might do social harm in making food cheaper in an already obese society.

A key learning from this concept is that those who are others-focused will be rewarded more richly by the market than those who are self-focused4. We have the idea today that work is about self-fulfillment or self-actualization, and this is true to a limited degree, in that one should stay away from work that one would hate or is unsuited to do. Some, however, remain trapped in a desire loop against tremendous odds.

The Costs of Self-Indulgence

I remember looking over the list of majors and starting salaries at Texas A&M a few years ago. I recall seeing a new major, Visualization, under the school of architecture. This coursework involved learning digital three-dimensional modeling and animation with cutting-edge software. A few graduates had been picked up by Pixar and other top players in the industry. Cross-referencing the career center’s salary survey, I found that Visualization was among the lowest starting salaries of any field, down there with obscure, low-demand degrees like art history.

Visualization, despite the high skill level of graduates, had low salaries because its hiring base was the entertainment industry, a part of a constellation of the economy I call the “glamour industries:” sports, music, fashion, acting, film, and art. It’s not that the people that do these things don’t create value, they most certainly do and much of the richness of life would be lost without their contributions. The issue is at the margin. The work is so personally fulfilling (or perceived to be) that way more people desire to work in these industries than are needed to meet demand. The result is that the median earnings of sports players, musicians, models, actors, artists, and film directors is nearly zero.

Only those with extreme outlier giftedness, connections to the industry, and a good bit of luck have any hope of being paid for this work. As the ghost of Hank Williams told David Allen Coe in the classic country song, “if you’re big star bound, let me warn ya it’s a long hard ride.” The market is providing a very clear signal to 99% of hopefuls: “We have enough of this, find something else to do.”

Because of the self-indulgent mentality of our society, most of the opportunities are now in areas that are both boring and complicated. This matrix contrasts “simple vs. complicated” with “exciting vs. boring.”

The upper left part of this matrix concerns things that are simple and exciting, like a theme park vacation, which are forms of leisure for which one must pay to do, not get paid to do. The upper right concerns the glamour industries, described previously, along with fields that provide a great degree of personal fulfillment or status like journalism or academia; because the supply of people doing these jobs exceeds demand, pay is low and most simply can’t find a steady job doing this work. Much of the power of the Left comes from the dissatisfied overeducated, who pursued soft hobbies as careers and rage at their fellow citizens who do not care to pay them when they ignore market employment signals.

The lower left quadrant consists of “unskilled” labor, which is normally low-paid, but because of its low status and the scarcity of people willing to work, is usually better-paid than glamour industries. Roofers and drywallers out-earn adjunct professors and the modal video editor. But the highest-earning are those fields that are both boring and complicated in the lower right quadrant. I’m thinking of my engineer friends who work in local refineries, who sucked it up to study hard things needed by the economy and are now rewarded. Lucky for them, many have atypical personalities where they do find tedious, boring work interesting, but they’re well-paid because of their rare skills and lack of personal vanity in pursuing a career to support their families5.

This may seem a dismal way to look at the world, and indeed economics has been called “the dismal science.” Reality has this way of not conforming to our hopes and dreams6.

Another more liberating perspective is that the market gives us objective guidance that is independent of our thoughts and feelings. Those things that animate me as a human being - perhaps being a husband, father, scholar, musician, or artist - have an existence independent of the market. The market merely demands that I contribute in some way, in some part of my life, that other people value based on price and profit signals. It is loving my neighbor as myself. Just as I want others to provide for my needs, as expressed by my choices in spending my money, I must do so for others.

There is, however, a fundamental tension between what it means to be fully human and maximizing one’s contribution to the modern economy. As Robert Heinlein said, “A human being should be able to change a diaper, plan an invasion, butcher a hog, conn a ship, design a building, write a sonnet, balance accounts, build a wall, set a bone, comfort the dying, take orders, give orders, cooperate, act alone, solve equations, analyze a new problem, pitch manure, program a computer, cook a tasty meal, fight efficiently, die gallantly. Specialization is for insects.”

It is undeniable we were built to be generalists, and the multitude of talents required to run a subsistent, independent farm, as 90% of humans did before modern times, required all of our many gifts. We might have lived on the brink of starvation, but it was a world where every human ability mattered.

This is the appeal of reactionary, romantic economic thinking, in that while we were poorer, we were undoubtedly happier in the old way of doing things, as long as we were spared calamity. It was a world before the war between the sexes, where a husband and wife engaged in productive work on the same land, each laboring vigorously in ample sunshine and fresh air, one with gross strength and the other with dexterous finesse, complementary gifts crafted by God in harmony to support their common household. It was also a world where children were economic blessings: extra laborers to increase yield and prosperity7.

Nevertheless, capitalist prosperity requires technological advancement, which requires specialization of labor. This difference between what we were designed to do for much of our history and what we do now is the source of much of the unhappiness of modern life despite our prosperity. Thankfully, I believe this is a much more solvable problem than the wages of poverty and struggle faced by our ancestors, and we ought to take action as necessary to solve it. Daily, vigorous exercise and long walks outdoors to cater to our ancestral design are a small price to pay for essentially zero risk of seeing our children starve or die of now-preventable diseases.

The problem can be overstated. Karl Marx thought the “alienation” of labor would inevitably lead to a communist revolution. An egghead himself, he could not imagine laborers being content to turn screws on an assembly line. Contrary to Marx, however, the average people seem to very much enjoy manufacturing jobs, as however minute the labor specialization, the physical, tangible nature of the work is fulfilling.

What people seem to find truly alienating is the experience of office life, of staring at screens and abstractions of physical production all day. The success of Dilbert and movies like Office Space crystallize this fundamental dissatisfaction. The management class itself might be partly a manifestation of a desire among office workers to avoid the tediousness of actual white collar work and instead get paid to pontificate in useless meetings all day. So it is not Marx’s mindless mechanics turning bolts on an automobile assembly line who became a dissatisfied proletariat, but rather disaffected paper pushers.

Discount Rates

Regardless of our personal struggles, the market marches on with its pricing and profit signals. The more we can think about marginal production, i.e. what does the world need incrementally right now, the more successful we will be in the economy. But before our picture of the fundamentals of economics can be complete, we must discuss discount rates. Discount rates reflect our preference for consumption now or consumption later. It adds the dimension of time to the profit signals of the economy.

A business should be “long-term greedy.” That is, short-term profits can often be traded for long-term profits. It’s a crass way to describe actions in the economy, but it’s a shorthand that helps us think about our self-interest in a consistent framework. In the context of economic trade and cooperation, the invisible hand of capitalism means being “long-term greedy” is also the best and highest way to serve others.

One way we can be long-term greedy is in how we manage customer relationships. Imagine a vendor with a relationship with a long-standing customer, and suddenly there is a supply disruption for a certain good the vendor provides to the customer. Short-term greedy would be to raise prices on the customer to extract the most profit out of the relationship right now.

Long-term greedy would be to smooth out some of the fluctuations in supply and demand for the customer to maintain a long-term, mutually trusting relationship. In other words, we are saying the lifetime profit this customer will generate for us under a regime of stability and cooperation will exceed the short-term profit from milking the maximum out of each individual transaction, which may cause the customer to take business elsewhere when he has the opportunity.

But there has to be a limit to this kind of thinking. Would we accept $105 a century from today rather than $100 today? Probably not, even if inflation were not a concern. It is rational to prefer profit today to profit tomorrow, and the mathematical relationship between the two is called the discount rate.

The most elegant way to determine discount rates is with an internal rate of return analysis. This type of analysis is mathematically complex but easy with modern spreadsheets. IRR analysis can be used to analyze almost any decision that involves tradeoffs of expenses now for payoffs later.

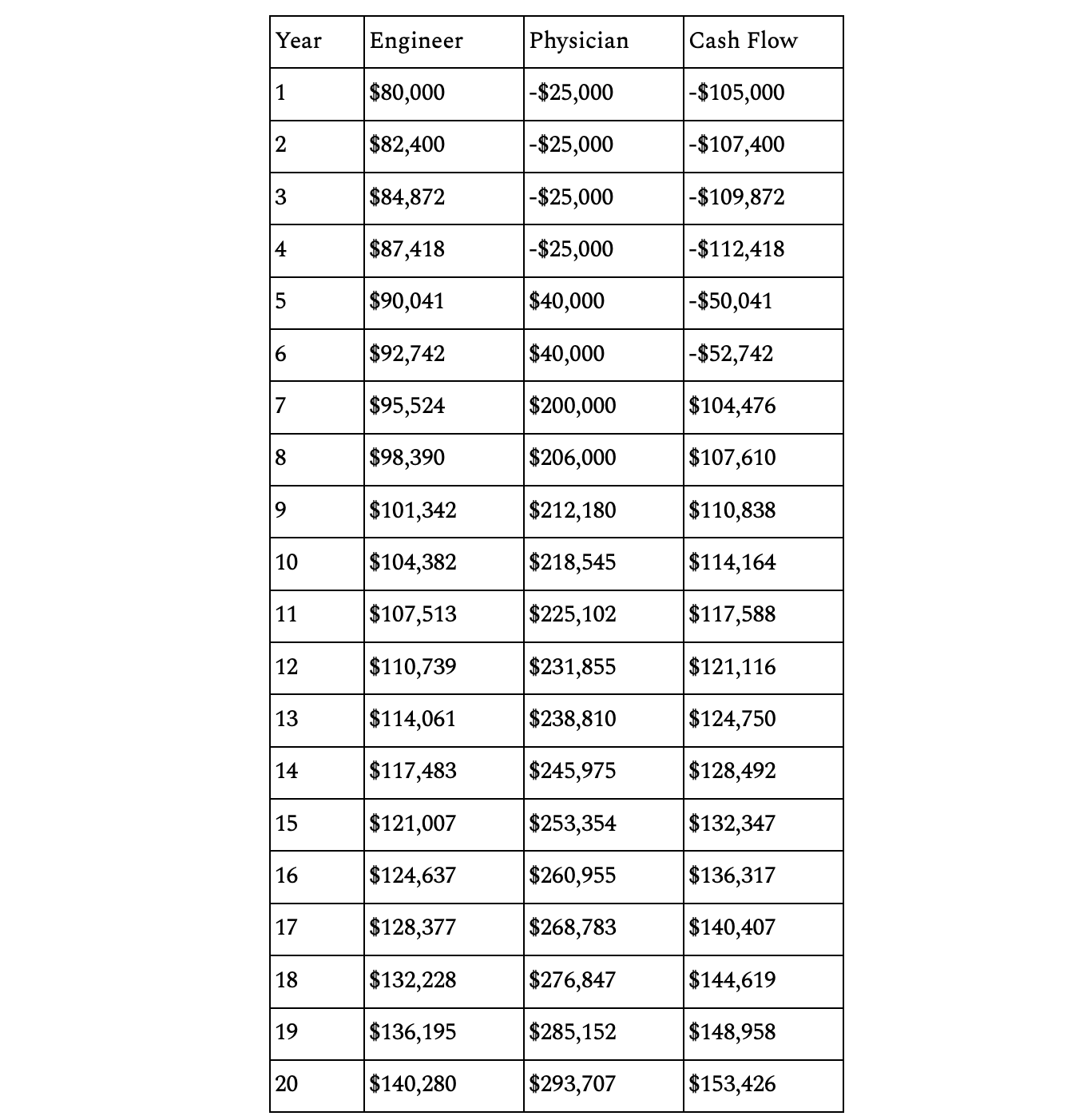

As an example, let’s consider a high school student who is talented in math and science and who is comparing a career as an engineer to that of a physician. She knows being a physician pays more, but also that she will run up expenses and have lost earnings from the extended time of education. What exactly is her return on investment for going to medical school?

We conduct an IRR analysis between two scenarios by computing the difference in each annual period in expenses and income (as this was written several years ago, these numbers are a little dated relative to post-Covid currency devaluations). Let’s assume that undergraduate costs are identical, so we will begin our comparison with graduate school. Consider the following table:

This table shows my simplified estimate of the incomes and expenses associated with the two career paths. The result is a series of annual cash flows over time. Notice how cash flow is heavily negative early on for the physician, in loss of foregone wages and extra tuition. When we apply the IRR() formula to the final row, we compute an internal rate of return of 13%. That is, a doctor’s education pays a 13% return, over 20 years, compared to being an engineer. However, they only break even after ten years, at age 32 or so, and most of the return is backloaded, when in the 40’s and beyond. If our doctor wishes to have a family, engineering may be the superior choice.

Discount rates and internal rates of return allow us to quantify the benefits of being long-term oriented in our pursuit of profits. But what discount rate should an operating business demand on investment? This is not an easy question to answer. To some degree, it involves predicting the future, but several present facts impact the analysis:

The current “risk-free” interest rate, typically the yield of the 10-year United States treasury. This is somewhat of a misnomer, as bonds paid by fiat currencies are subject to inflation at the government’s whim.

Alternative investments available for cash distributed from the business. For example, if 10% returns can be earned in a safer, more stable investment, even if not risk-free, this is superior to earning 10% inside a small business exposed to more risk.

The inherent and inevitable overconfidence, underestimation of costs, and overestimation of benefits of a business’ management.

The last factor is partially due to human frailty — we tend naturally to be overconfident in projects we wish to pursue — but also due to the inherent tension between non-owner management and owner’s capital, called the principal-agent problem.

Someone earning a salary from a business has a different set of incentives than someone earning a portion of profits. The salary is “sticky” and unlikely to change unless the employee is terminated or promoted. This disincentivizes taking moderate, rational risks that perhaps need to be taken and incentivizes low-risk, but capital-intensive projects that naturally support a promotion or else, in a startup, large, capital-intensive risks with lottery-ticket-type payoffs.

A manager on salary is incentivized to grow his or her team and company resources under management for the sake of small, predictable returns on investment or large home runs that may not be rational from an owner’s perspective. This is because salaries (including creditable experience for future job opportunities) are usually benchmarked to the size of a team or budget, or the ambition of the project, not the profits that result from them. People from failed startups are usually easily able to find new jobs because they at least have experience managing something “at scale,” even if that scale blew through millions of investor cash.

For this reason, most mature, extremely large businesses demand internal returns on investment of at least 20% over the risk-free rate for proposed projects. Such a return compensates for overconfidence and principal-agent distortions. A smaller, less mature business should demand something higher, perhaps 30% over the risk-free rate. This is because small businesses have inherent systemic risks that cannot be adequately accounted for in project scope.

Discount rates also often help us reconcile what feels morally right with what is actually economically right. A key teaching of the Reformation’s approach to money is that in the long term, on average, doing the right thing is also what is in our self-interest8. God’s laws are primarily for our benefit, not for demonstrative acts of asceticism to prove our devotion.

Profit, properly discounted over time, is the signal by which capitalism directs the activities of private parties to serve their fellow man in the best way possible. It is a fundamental belief of mine that, much of the time, producing and selling does much more social good than charity. Products people need and that do them well, that people choose to buy with their own scarce money, allocate limited resources of labor and material better than any charitable project could hope to match.

On the other side of the balance sheet, the compensation to employees, in supporting families and honest labor, does more for the dignity of men and women than charitable gifts. The incredible wealth we enjoy today did not come from charities. It is capitalism, the applied law of God enabled by the common grace radiating from the core gospel, that alone is eliminating severe poverty, reversing the extreme scarcity of the fall of man, and directing the creative energy of the talented and ambitious into plowshares that provide rather than swords that exploit.

The Dignity of Work

There is great meaning and dignity in our economic work when we properly see its scope. Even our most frivolous purchases serve this purpose. When you buy a plane ticket for personal travel, in the cockpit sits a pilot, who has probably dreamt of flying since childhood. Pilots famously say that it’s the best job because, from their perspective, they never have to work a day in their life. One is either not working, or flying an airplane, which to a true pilot is joy, not labor. In this beautiful system, a human being is lifted up because other human beings want to go on vacation.

This meaning and dignity extends not only to business owners but anyone who labors for a living. The surplus of your employment creates opportunities for employment of others, in a virtuous circle of cooperation and, dare I say, love.

The most elegant explanation of the purpose of money is to provide a temporary store of value as people trade productive assets. See here for the best explanation I’ve seen that is contrarian to both gold and crypto bugs: https://lt3000.blogspot.com/2021/04/crypto-mania-is-back-crypto-vs-fiat-and.html. Unfortunately, I think the author fails to appreciate that democratic governments will inevitably debase a fiat currency beyond a reasonable inflation rate due to political pressures. Somewhat deflationary hard money may be necessary due to man’s fallen nature. I expand on this in my post considering the prospects of Bitcoin.

The benefits of a social welfare system are part of the inducement to immigrate, essentially a wage subsidy, which lowers costs for employers and customers while everyone else pays for the costs, net of taxes, of education, health care, law enforcement, etc. A better system, if immigration were judged necessary, would require employers to reimburse taxpayers for any benefits received by their discretionary immigrant workers, along with indemnifying citizens and civil authorities for any torts or law enforcement costs related to acts committed by workers while in the country. If these actual costs and risks were borne by the employer, most would find raising wages to attract sufficient domestic labor would be more cost-effective.

Agrarian life also involved a great degree of romanticism, i.e. hobby-like aspects that provide non-economic compensation. Historically, the “landed gentleman,” in its association with aristocracy, provided a great deal of status as well — in England, often “new money” merchants would buy money pit country estates to show they had “arrived” — and it took quite a bit of time for people to accept the post-industrial-revolution economic message. Much of the success of immigrants in the early 1800s and 1900s was due to old-stock Americans pursuing this agrarian ideal despite falling crop prices. William Jennings Bryan’s political career was the expression of farmers politicizing their economic frustrations in pursuing dead-end, low-yield investments in land.

These ideas can be applied outside of economics as well. In the evangelical world, many more Christians seem to be “called” into full-time ministry than there are positions available. The question is not whether ministry is good or bad, but whether the church benefits by having one more minister and one less layperson. Is their marginal choice for vocational ministry better for the church’s mission than working in the normal economy and giving to better support those already in ministry?

To be fair, guidance counselors and the university industrial complex bear a lot of responsibility for suckering 17-year-olds into entering low-demand fields based on an immature student’s “passion” for photography, literature, or other activities best considered a hobby. This is not to say I’m a total Philistine in this area; we need writers, poets, and philosophers, just not very many of them relative to the population. Historically, people who made a career of their hobbies, say being a historian or museum curator, tended to have family money (i.e. trust funds or the like) or a wealthy patron such that they were economically indifferent to the field’s compensation. For students without family money, it is malpractice to recommend entering low-compensation fields. I immensely enjoy writing this Substack discussing philosophy, economics, health, and religion, but I don’t expect people to pay me for my scribbling. You might have noticed that the supply of opinions on the Internet vastly exceeds the demand!

I am reminded of the old John Adams quote, “I must study politics and war that my sons may have liberty to study mathematics and philosophy. My sons ought to study mathematics and philosophy, geography, natural history, naval architecture, navigation, commerce and agriculture in order to give their children a right to study painting, poetry, music, architecture, statuary, tapestry, and porcelain.” Adams here outlines the proper order of priorities multi-generational families ought to pursue: political freedom first, then economic freedom, then intellectual freedom for productive leisure.

The necessity, for most people, to study economically valued fields is also my weird reason for supporting classical education in K-12. With university liberal arts degrees largely woke, unvalued in the marketplace, and overpriced, K-12 is the least opportunity cost venue for teaching them and capturing their value for creating well-rounded students prior to economically-informed specialization.

Something I’ve recently considered is why the most talented people in finance out-earn those, like engineers, who work in the “real economy.” There are exploitive aspects to this, no doubt, largely due to fiat money printing, but it’s also possible that a significant part of their value-add is allocating capital. Marginal economics means sometimes being a middleman who makes the economy more relatively efficient moving resources around provides more value at the margin than the absolute producers of real goods. This is particularly subtle when one is an investor in established businesses. At the highest abstract level, a buyer of a stock or bond is providing marginal capital to a business enterprise. If there was no bidder, the industry would cease to exist.

By contrast, children today have negative economic externalities. Parents bear the entire cost for their education and nurture, benefiting the rest of society, yet receive no return for their investment other than personal fulfillment. Some have suggested various schemes to account for this externality. The most elegant proposals in my view enhance parental social security payments based on the direct taxes paid by their children. If you raise productive children, you enjoy a more comfortable retirement, but of course, this does little to help when parents need extra income to offset children’s expenses. The most effective proposals probably involve something like a highly enhanced non-refundable Earned Income Tax Credit for married households with children.

This is a general statement of averages. The converse absolute is not true, i.e. that which is in our self-interest is not automatically morally right, particularly in meeting legitimate obligations. A righteous man “swears to his own hurt and does not change.”